Blockchain is a digital database that is shared among a network of computers. It is used to store information electronically and is well-known for its role in cryptocurrency systems such as Bitcoin, where it helps maintain a secure and decentralized record of transactions.

Introduction

Blockchain is a decentralized technology developed by Satoshi Nakamoto that enables the distribution of digital information. It is made up of a network of computing nodes and is known for its impressive characteristics, including durability, robustness, transparency, and incorruptibility. It is primarily used to manage Bitcoin transactions through a global network of computers. Still, it has the potential to be applied in a variety of business contexts, such as crowdfunding, smart contracts, and supply chain auditing.

Benefits and features of blockchain technology

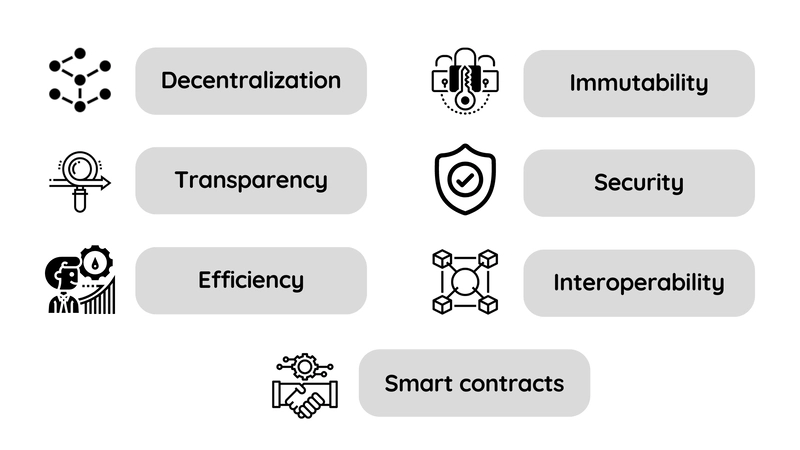

Blockchain technology has several key benefits and features that make it attractive for various applications:

- Decentralization: One of the main benefits of blockchain is that it is decentralized, meaning that a single entity or authority does not control it. Instead, it is maintained by a network of computers, or nodes, that work together to validate and record transactions. This decentralized structure makes it resistant to tampering or fraud.

- Immutability: Once data has been recorded on a blockchain, it is very difficult to change or alter. This feature, known as immutability, ensures that the integrity of the data is maintained and that it can be trusted.

- Transparency: Blockchain technology is transparent, meaning that all transactions and data stored on the blockchain are visible to all users. This makes it easier to track and verify the authenticity of transactions, increasing trust and accountability.

- Security: Blockchain uses cryptographic techniques to secure the data stored on the blockchain and to ensure that transactions are valid. This makes it resistant to cyber-attacks and helps to protect against fraud and unauthorized access.

- Efficiency: By automating certain processes and eliminating the need for intermediaries, blockchain technology can increase the speed and efficiency of transactions and reduce the costs associated with them.

- Interoperability: Blockchain technology can facilitate the exchange of data and assets between different systems and platforms, enabling greater interoperability and reducing the complexity of certain processes.

- Smart contracts: Blockchain technology can enable the creation and execution of smart contracts, which are self-executing contracts with the terms of the agreement between buyer and seller being directly written into lines of code. Smart contracts can help to reduce the risk of fraud and increase the efficiency of specific processes.

Proof of the concept of a distributed ledger

A distributed ledger is a type of database that is decentralized and distributed among a network of computers or nodes. It is designed to be transparent, secure, and immutable, and it allows multiple parties to record and track transactions without the need for a central authority.

One way to demonstrate the concept of a distributed ledger is to create a simple blockchain using a programming language such as JavaScript. Here's an example of how you might do this:

const crypto = require('crypto');

// Define the Block class

class Block {

constructor(data, previousHash) {

this.timestamp = Date.now();

this.data = data;

this.previousHash = previousHash;

this.hash = this.calculateHash();

}

calculateHash() {

return crypto.createHash('sha256')

.update(this.timestamp + JSON.stringify(this.data) + this.previousHash)

.digest('hex');

}

}

// Define the Blockchain class

class Blockchain {

constructor() {

this.chain = [this.createGenesisBlock()];

}

createGenesisBlock() {

return new Block('Genesis Block', '0');

}

getLatestBlock() {

return this.chain[this.chain.length - 1];

}

addBlock(newBlock) {

newBlock.previousHash = this.getLatestBlock().hash;

newBlock.hash = newBlock.calculateHash();

this.chain.push(newBlock);

}

isChainValid() {

for (let i = 1; i < this.chain.length; i++) {

const currentBlock = this.chain[i];

const previousBlock = this.chain[i - 1];

if (currentBlock.hash !== currentBlock.calculateHash()) {

return false;

}

if (currentBlock.previousHash !== previousBlock.hash) {

return false;

}

}

return true;

}

}

// Create a new blockchain

const blockchain = new Blockchain();

// Add some blocks to the chain

blockchain.addBlock(new Block('First block', blockchain.getLatestBlock().hash));

blockchain.addBlock(new Block('Second block', blockchain.getLatestBlock().hash));

blockchain.addBlock(new Block('Third block', blockchain.get

Process of adding new blocks to the chain

The process of adding new blocks to a blockchain typically involves the following steps:

- A new transaction is initiated by a user. This could be a financial transaction, such as the transfer of cryptocurrency, or the exchange of other types of data or assets.

- The transaction is broadcast to the network of nodes that make up the blockchain.

- The nodes verify the transaction to ensure that it is valid and complies with the rules of the blockchain. This may involve checking the digital signature of the user who initiated the transaction to verify their identity, as well as checking the availability of the assets being transferred.

- If the transaction is valid, it is added to a pool of unconfirmed transactions, also known as the mempool.

- Miners (in the case of a public blockchain) or the nodes (in the case of a private blockchain) select transactions from the mempool to include in the next block. The selection process may be based on various factors, such as the transaction fee offered by the user or the priority of the transaction.

- The selected transactions are added to a new block, along with a timestamp and a unique code, known as a hash, that links the block to the previous one in the chain.

- The miner or node attempts to solve a complex mathematical problem in order to validate the block and add it to the chain. In a public blockchain, the first miner to solve the problem is rewarded with a small amount of cryptocurrency.

- Once the block has been validated and added to the chain, the transactions it contains are considered confirmed.

function addBlock(blockchain, newBlock) {

// Validate the new block

if (isValidNewBlock(blockchain, newBlock)) {

// Add the new block to the blockchain

blockchain.push(newBlock);

} else {

console.log('Invalid block. Not added to the blockchain.');

}

}

function isValidNewBlock(blockchain, newBlock) {

// Check that the new block has a valid hash

if (calculateBlockHash(newBlock) !== newBlock.hash) {

return false;

}

// Check that the new block has a valid previous block hash

const previousBlock = blockchain[blockchain.length - 1];

if (newBlock.previousHash !== calculateBlockHash(previousBlock)) {

return false;

}

// If the new block passes all checks, it is valid

return true;

}

function calculateBlockHash(block) {

// Calculate the hash of the block data using a cryptographic hash function

return crypto.createHash('sha256').update(block).digest('hex');

}

This process may vary slightly depending on the specific blockchain platform being used.

Role of miners and consensus algorithms

Miners and consensus algorithms are key components of many blockchain platforms and play important roles in the process of adding new transactions to the blockchain.

What do miners do in blockchain?

Miners are responsible for validating transactions and adding them to the blockchain in a public blockchain. They do this by competing to solve a complex mathematical problem, and the first one to solve it is rewarded with a small amount of cryptocurrency and the right to add the next block to the chain. This process is known as mining.

What does consensus do in blockchain?

Consensus algorithms are rules that govern how nodes reach an agreement on the state of the ledger in a blockchain. They are used to ensure that all nodes on the network agree on the validity of transactions and the current state of the blockchain. There are various types of consensus algorithms, including proof of work, proof of stake, and delegated proof of stake.

function proofOfWork(block, difficulty) {

// Find a number that, when hashed with the block data, produces a hash

// with `difficulty` leading zeros

while (true) {

block.nonce++;

let hash = hashBlock(block);

if (hash.substring(0, difficulty) === '0'.repeat(difficulty)) {

return block.nonce;

}

}

}

function hashBlock(block) {

// Hash the block data using a cryptographic hash function

return crypto.createHash('sha256').update(block).digest('hex');

}

Different types of the blockchain

There are three main types of blockchains: public, private, and consortium. Each type of blockchain has its own advantages and disadvantages, and the most appropriate type will depend on the specific needs and goals of the application.

| Public blockchains | Private blockchains | Consortium blockchains |

|---|---|---|

| Public blockchains are open to anyone and are secured through the mining process. | Private blockchains are restricted to a specific group of users and are not secured through mining. | Consortium blockchains are a hybrid of public and private blockchains. |

| Examples of public blockchains include Bitcoin and Ethereum. | Used in industries such as finance and healthcare, where the need for security and privacy is high. | Hyperledger is an example of a consortium blockchain. |

Applications of blockchain

Blockchain technology has the potential to revolutionize a wide variety of industries and applications. Here are a few examples of how blockchain is being used or has the potential to be used:

- Cryptocurrencies: One of the most well-known applications of blockchain is in the creation of digital currencies, such as Bitcoin. Blockchain allows for the secure, decentralized tracking of digital currency transactions.

- Supply chain management: Blockchain can be used to track the movement of goods through a supply chain, providing transparency and enabling more efficient and accurate tracking of products.

- Identity verification: Blockchain technology can be used to create secure, digital identities that can be used to verify the identity of individuals or organizations.

- Smart contracts: Blockchain technology can be used to create self-executing contracts that are automatically triggered when certain conditions are met.

- Voting systems: Blockchain can be used to create secure, transparent voting systems that can be used in elections or decision-making processes.

- Health records: Blockchain can be used to securely store and manage electronic health records, enabling more efficient and accurate tracking of patient data.

- Real estate: Blockchain can be used to track property ownership and transfer, streamlining the process of buying and selling real estate*.*

- Education: Blockchain can be used to track and verify educational qualifications, making it easier for employers to verify the credentials of job candidates.

The future of blockchain:

Blockchain technology is still in its early stages, and it is difficult to predict exactly how it will evolve in the future. However, it is likely that blockchain will continue to grow in popularity and usage as more industries and applications adopt it. Some potential future developments for blockchain include:

- Increased adoption: As more industries and organizations become aware of the benefits of blockchain, it is likely that adoption will continue to grow.

- Development of new consensus algorithms: Consensus algorithms play a crucial role in the security and reliability of blockchain technology. As the technology continues to evolve, it is likely that new consensus algorithms will be developed to improve the performance and scalability of blockchain systems.

- Improved scalability: One of the main challenges facing blockchain technology is scalability – the ability to process a large number of transactions quickly. As the technology develops, it is likely that new solutions will be found to improve the scalability of blockchain systems.

- Integration with other technologies: Blockchain technology is likely to be integrated with a variety of other technologies, such as artificial intelligence and the Internet of Things, to create new and innovative solutions.

- Increased regulation: As blockchain technology becomes more widely used, it is likely that it will be subject to increased regulation to ensure its proper use and protect users.

- Wider use of decentralized applications: Decentralized applications (dApps) are applications that are built on top of blockchain technology and are decentralized, meaning they are not controlled by a single entity. It is likely that the use of dApps will continue to grow as more people become aware of their benefits.

Wrapping up

Blockchain technology has the potential to transform a wide variety of industries with its decentralized, secure, and transparent nature. Its potential applications include cryptocurrency, supply chain management, identity verification, smart contracts, voting systems, health records, real estate, and education. As technology continues to mature and be adopted by more companies and organizations, we can expect to see an increasing number of practical applications. It is important for individuals and companies to stay informed and embrace blockchain technology to take advantage of its benefits.

Top comments (0)