Financial services is at a crossroads. Some organisations have made a paradigm shift using serverless to create new digital business models and others have ignored digital transformation and are falling behind customer expectations with traditional bricks and mortar propositions bolted together with rudimentary digital offerings.

Many organisations are struggling to even make the decision to change to new business models. Traditionally, financial service organisations struggle with business model innovation have an outdated matrix structure. In the book, Strategic management: A competitive advantage approach; Fred and Forest David point out that matrix structures “replace single lines of authority with multiple cross-matrix relationships….it will take longer to reach decisions because of bargaining between the managers of different dimensions”.

In the financial services industry, most organisation’s business models are similar to Chris Skinner @ Finanser.com’s description of being based on an “industrial economy (which) was all about scale… But these investments in scale in the digital age are quickly moving… to sources of competitive disadvantage”. Serverless enables tech resources to be available cheaply to everyone meaning that scale doesn’t matter. A business can rent as little or as much digital technologies as it needs, conferring little scale advantage in running a massive operation.

What analysis should you be carrying out for a new digital business model?

Finextra describe how: “the traditional model of banking is being broken up and shrinking revenue streams will need to be replaced with alternatives. We are moving to a platform marketplace where different parties are interacting seamlessly… Not only are we dealing with tech and cost challenges but also the challenge to preserve and grow our business.”

In the article ‘How DBS pursued a business strategy‘, DBS Bank realised that: “IT needs to be pervasively embedded in every aspect of a bank and be an integral part of business strategy”. This is well illustrated in the diagram below:

DBS Bank Business Strategy Diagram

In the 11FS Blog – Banking Battlefield: Winning the War for Customers, David M. Brear recognises the new market dynamics.

Diagram of market dynamics in the banking industry

Digital business model of the banking industry

“Everyone is trying to get to the top right of this (digital business model) diagram. Everyone wants the most customers and the most sophisticated IDS (intelligent digital services). Incumbent banks have the customers but they need the tech, new challengers have the tech but not the customers, and the big tech companies seemingly have everything they need to be a real threat, if and when they start offering banking services.”

Too many organisations are focused on operational efficiency rather than building their digital business model. According to Frery, in ‘The Fundamental Dimensions of Strategy‘, MIT Sloan Management Review: “cost-cutting techniques cannot provide long term competitive advantage.”

Instead, we must take heed of FinTech Futures “….due to the speed of development in technology and the range of offerings in the market, to succeed as a business you need to continue innovating… we are referring to a combination of high-quality data, processes, tools, and skills married with an institutional culture which encourages experimentation, learning, and the perpetual improvement of products and services”

As a general approach, financial service orgs should study DBS Bank’s case study. It shows how DBS: “gradually built up the necessary capabilities to pursue a successful digital business strategy”

DBS Bank's digital transformation plan

What are the strategic choices open to organisations?

Create new Digital Business Model(s): Finanser Website (2018): “In the world of cloud computing, IT resources are available cheaply to everyone meaning that ….scale doesn’t matter…. In this digital age, the scaled business model is likely to lead to the double whammy of failing to spot new trends and the impossibility of catching up.”

Partner with tech: As Duena Blomstrom points out in her book ‘Emotional Banking‘: “FinTech start-ups that initially declared themselves as challengers have…either sold their company to banks (such as Bank Simple and BBVA) or have partnered with them (such as Moven and TD Bank) to supply them with technology and winning front-end propositions and the discourse has changed from seeing FinTech as competitive to seeing it as enabling.”

Enable Data & Fix Culture: Duena Blomstrom pinpoints the issues perfectly in her book: “The real reason why we as consumers didn’t see any of the benefits of handing over so much data is twofold: one is bank culture and the second one is technology impotence.”

Revise Business Cases: Teece in his article, ‘Dynamic capabilities and strategic management‘, shows that: “…the conclusion by established companies that investing aggressively in disruptive technologies is not a rational financial decision…First, disruptive products are simpler and cheaper; they generally promise lower margins, not greater profits. Second, disruptive technologies typically are first commercialized in emerging or insignificant markets. And third, leading firms’ most profitable customers generally don’t want, and indeed initially can’t use, products based on disruptive technologies. Hence, most companies with a practiced discipline of listening to their best customers and identifying new products that promise greater profitability and growth are rarely able to build a case for investing in disruptive technologies until it is too late.”

Move from selling products to serving customer needs: Blomstrom: “From a customer point of view the true Nirvana of banking would…be if it became utterly invisible and kept serving us flawlessly in the background, thus empowering our Money Moments (the life moment that money will facilitate)”

Build true Brand Equity across the customer experience, beyond advertising: Blomstrom: “recognize the value of being a brand and…..change the culture to accomplish that….banks can still win the battle for the consumer. All they need to do is grow in knowledge, courage and passion”.

Exploit emerging technologies: Finextra Webinar: “Cost efficiencies from cloud technology and stability mean that N26 don’t need to maintain their own data centres….. they commoditise the infrastructure in order to focus on the customer “

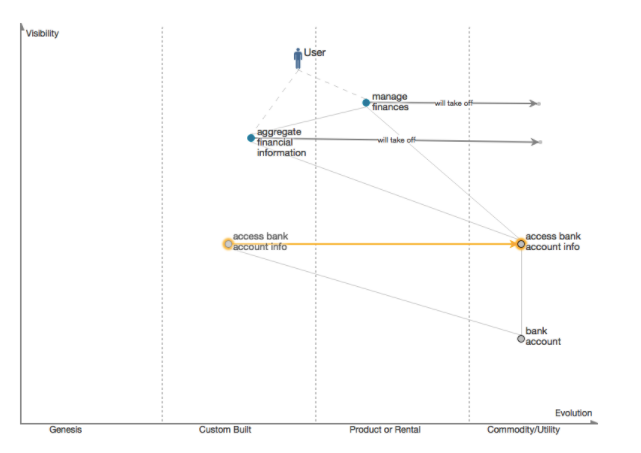

Perform Wardley Mapping to Identify True Value Proposition: Teece: “Our approach is especially relevant in a Schumpeterian world of innovation-based competition, price/performance rivalry, increasing returns, and the ‘creative destruction’ of existing competences.”

Wardley Map of the Future of Banks

Conclusion:

DBS Bank managed to analyse the right issues and examine the right problems: “Thus, banks need to ask themselves which parts of the business should we keep in-house and at the forefront of innovation; should we collaborate with strategic partners on; should we seek to acquire new capabilities or should we strategically lag as a late adopter”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Top comments (0)