some time is hard to back test your strategy with back test library i made easy . with 3 lines of code you can back test and see result of your strategy.

https://github.com/xibalbas/signal_backtester/

support the project with your stars :))

what is Signal Backtester?

it is a tiny backtester Based on Backtesting Lib .

easiest way to backtest your generated signal. just need a csv file contain candleStick informations. OHLCV + signal

why??

some time writing good backtest for a strategy is not too easy . and you may have some challenge with backtest libraries.

so i decided to make a seprate repo for backtesting in easiest way.

what you need is a csv file contain signal column . for buy signal you should put 2, and for sell signal you put 1.

and good news is you did not need to write strategy for how trade we wrote it before you just choose yours and finish you did it :))

see Strategy guide.

First

prepare your data and prepare your signal .

you can write your strategy and generate signal like this

here is an example of generating signal for EMA cross strategy and show you how generate your signal .

our signal generate as new column signal in our data frame .

notice: your data set column should contain Date,Open, High, Low, Close, Volume,signal

import talib # notice you can install talib manually

import pandas as pd

def cross_EMA_signals(df, fast_period, slow_period):

"""_summary_

Args:

df (_type_): _description_

fast_period (_type_): _description_

slow_period (_type_): _description_

"""

signal = [0] * len(df)

df["fast"] = talib.EMA(df.Close, timeperiod=fast_period)

df["slow"] = talib.EMA(df.Close, timeperiod=slow_period)

for idx in range(len(df)):

if idx > slow_period:

if (

df.iloc[idx - 1].fast < df.iloc[idx - 1].slow

and df.iloc[idx].fast > df.iloc[idx].slow

):

# buy signal

signal[idx] = 2

if (

df.iloc[idx - 1].fast > df.iloc[idx - 1].slow

and df.iloc[idx].fast < df.iloc[idx].slow

):

# sell signal

signal[idx] = 1

df["signal"] = signal

df.to_csv("./final_dataset.csv")

df = pd.read_csv("./data.csv")

if __name__ == "__main__":

cross_EMA_signals(df, 15, 30)

second (Backtest in 3 line)

installation

pip install signal-backtester

make a backtest

from signal_backtester import SignalBacktester

dataset_address = "./final_dataset.csv"

backtest = SignalBacktester(

dataset=dataset_address,

strategy="two_side_sl_tp_reversed",

cash=100000,

commission=0.0005,

percent_of_portfolio=99,

stop_loss=1,

take_profit=2,

trailing_stop=3,

output_path="./result", # path of result files

)

backtest.run()

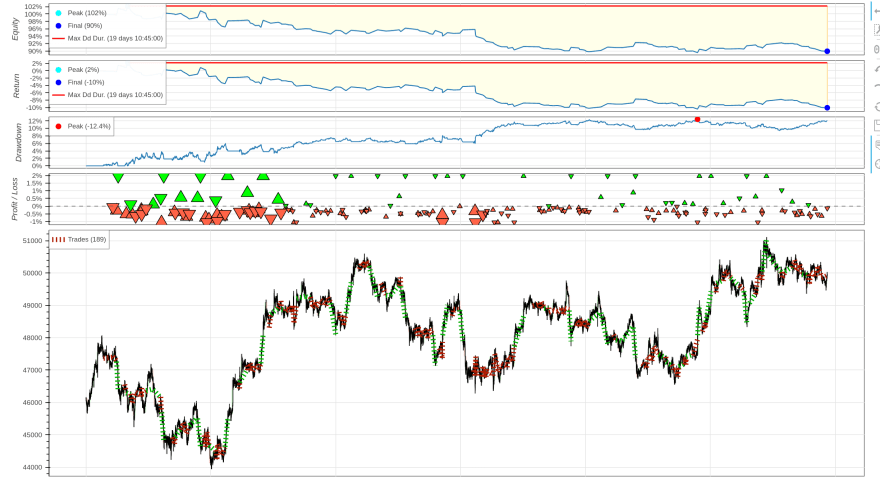

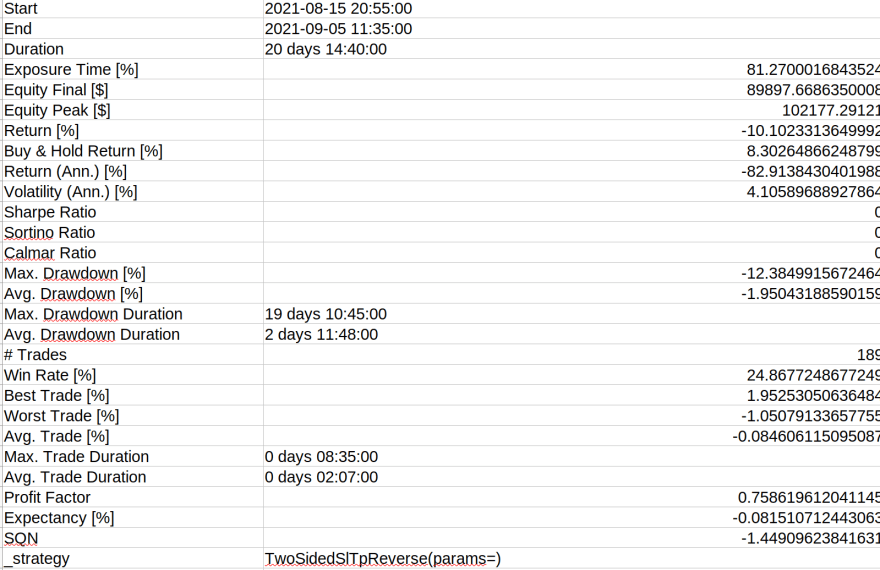

and simply get result of Backtesting lib:

final_report.html

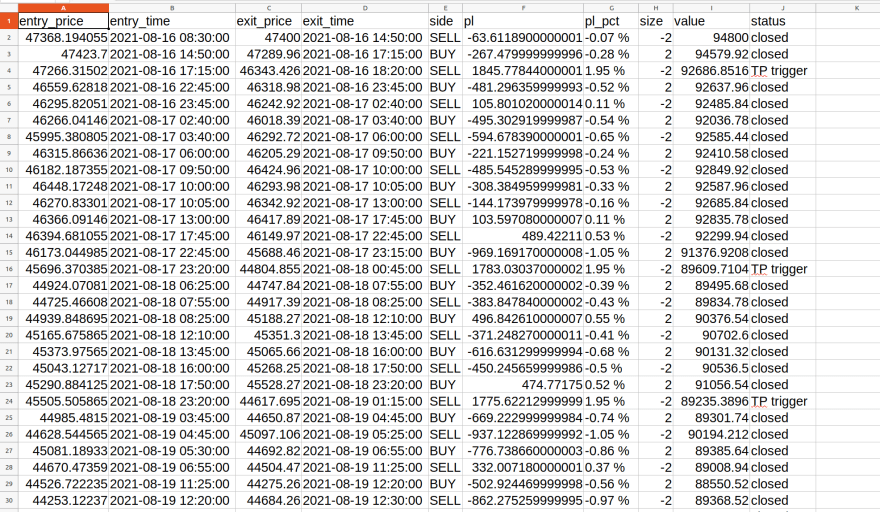

final_report.csv

order_report.csv

Top comments (0)