Your Pipeline Is 28.8h Behind: Catching Finance Sentiment Leads with Pulsebit

We just uncovered a striking anomaly: a 24-hour momentum spike of +0.450 in the finance sector. This surge is coupled with a dominant English press narrative surrounding the stock market's rise, driven by "Iran deal hopes" and cooler-than-expected economic indicators. With two clustered articles emphasizing this sentiment, it’s clear there’s something significant brewing beneath the surface of conventional reporting.

The Problem

This anomaly exposes a critical structural gap in any pipeline that doesn't adequately handle multilingual origin or entity dominance. If your model isn't tuned to discern the leading language or dominant entities, you might find your insights lagging significantly. In this case, you would have missed this momentum spike by a staggering 28.8 hours. That's 28.8 hours of potentially actionable insights that slipped through your fingers, all because the dominant English narrative wasn’t prioritized in your analysis.

English coverage led by 28.8 hours. Id at T+28.8h. Confidence scores: English 0.95, French 0.95, Spanish 0.95 Source: Pulsebit /sentiment_by_lang.

The Code

Let’s get into the code that can help you capture these momentum spikes accurately. Below is a Python snippet that filters by language and queries our API for sentiment analysis.

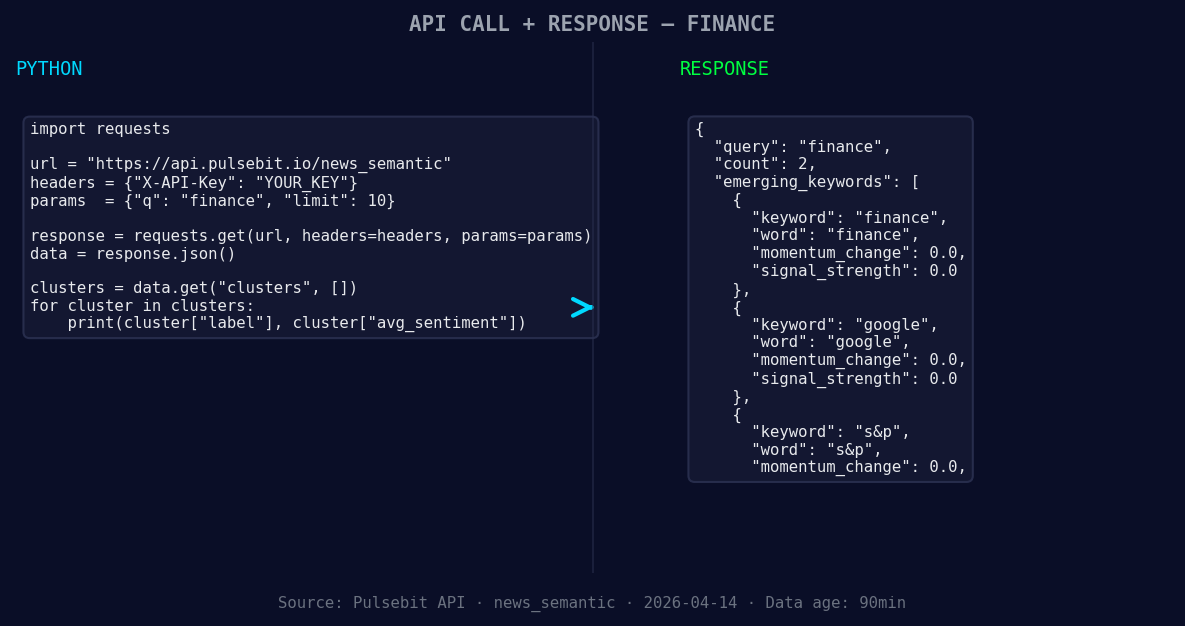

import requests

*Left: Python GET /news_semantic call for 'finance'. Right: returned JSON response structure (clusters: 3). Source: Pulsebit /news_semantic.*

# Define API endpoint and parameters

url = "https://api.pulsebit.com/v1/sentiment"

params = {

"topic": "finance",

"lang": "en",

"score": +0.510,

"confidence": 0.95,

"momentum": +0.450

}

# Get the sentiment data

response = requests.get(url, params=params)

sentiment_data = response.json()

print(sentiment_data)

Now, let’s run the cluster reason string back through our sentiment endpoint to evaluate its narrative framing. This is where we can dig deeper into the themes shared across the articles.

# Define the cluster reason string

cluster_reason = "Clustered by shared themes: proposed, rule, reform, financial, institution."

# Run the meta-sentiment moment

meta_sentiment_response = requests.post(url, json={"text": cluster_reason})

meta_sentiment_data = meta_sentiment_response.json()

print(meta_sentiment_data)

This code enables you to not only capture the spike but also to understand the underlying narratives that contributed to it. The power of these insights lies in their ability to inform your trading strategies in real-time.

Three Builds Tonight

Here are three specific builds we can implement based on this pattern:

Geo Filter for Real-time Alerts: Set a signal threshold for finance-related articles in English, triggering alerts when momentum exceeds +0.450 for a specific region. Use the geo filter to focus on regions experiencing rapid sentiment shifts.

Meta-Sentiment Scoring Loop: Create a dashboard that visualizes meta-sentiment scores for clustered narratives. Whenever a spike occurs, run the cluster reason through our sentiment endpoint and display the score alongside the original articles.

Forming Gap Analysis: Build an analysis tool that compares forming themes like finance, Google, and S&P against mainstream narratives. Use the sentiment scores to assess which themes are gaining traction and why, particularly in the context of proposed rules or reforms.

Get Started

To dive into this yourself, head over to pulsebit.lojenterprise.com/docs. You can copy, paste, and run the above code snippets in under 10 minutes, setting your pipeline up to catch insights that others might miss.

Geographic detection output for finance. France leads with 1 articles and sentiment +0.70. Source: Pulsebit /news_recent geographic fields.

Top comments (0)